You don’t need six figures in the bank to start investing in real estate. That’s the myth that keeps most people on the sidelines, and it’s flat wrong.

I’ve spent years working with first-time buyers and investors who assumed they were priced out. Some of them got started with a few hundred dollars in a REIT. Others bought a duplex with an FHA loan and let tenants cover most of the mortgage. The entry points are more varied than you’d expect.

This guide breaks down nine real ways to invest in real estate, from fully passive options to hands-on strategies. You’ll learn what each approach costs, how to pick the right one for your situation, and how to take your first step without making expensive beginner mistakes.

Also Read: Property Investment: Complete Guide to Real Estate Investing

What Is Real Estate Investing?

Real estate investing means putting money into property, whether that’s buying a rental home, investing in a real estate fund, or lending money secured by real estate. The goal is simple: make more than you put in.

There are four main ways real estate builds wealth. First, cash flow from monthly rent payments. Second, appreciation as property values climb over time. Third, equity buildup as tenants helps pay down your mortgage.

And fourth, tax benefits like deductions for mortgage interest, property taxes, maintenance, and depreciation. Most other investments give you one or two of those. Real estate can deliver all four at once, which is why it’s been a wealth-building tool for generations.

This article is for educational purposes only and does not constitute financial, legal, or investment advice. Real estate investments carry risk, including potential loss of capital. Consult a qualified financial advisor or real estate attorney before making investment decisions.

What Should You Consider Before Investing in Real Estate?

Buying your first investment property or putting money into a real estate fund shouldn’t be an impulse decision. Before you commit a dollar, get honest with yourself about four things.

- Budget and Capital: How much cash can you actually put toward an investment right now? For direct property purchases, you’ll typically need 15-25% down for an investment property loan, plus closing costs, insurance, and a cash reserve for repairs. FHA loans drop that to 3.5% if you’re willing to live in the property (more on that in the house hacking section). For REITs or crowdfunding, you might start with $100 or less.

- Time and Effort: Managing a rental property yourself might mean fielding tenant calls at 10 pm on a Saturday. Buying into a REIT takes about as much time as buying a stock. Be realistic about whether you want the landlord life or prefer something you can set and mostly forget.

- Risk Tolerance: A fix-and-flip project in a cooling market could lose you $30,000 or more if renovation costs spike or the property sits unsold. A publicly traded REIT might drop 15% in a stock market correction but recover within a year. Those are very different risks. Think about which scenario would keep you up at night.

- Knowledge and Education: You don’t need a real estate license to invest, but you do need to understand basic financial metrics like cap rates, cash-on-cash returns, and the 1% rule (more on those below). Resources like BiggerPockets, local real estate investor meetups, and books like “The Book on Rental Property Investing” by Brandon Turner are solid starting points.

I can’t tell you how many times I’ve seen someone rush into a purchase because a property “felt right” without running even basic numbers.

The investors I work with who do best aren’t the ones with the biggest bank accounts. They’re the ones who spent a few months learning the fundamentals before writing a single check.

What Are the Best Ways to Invest in Real Estate?

Not every real estate strategy is right for every investor. Your budget, schedule, and appetite for risk should drive your decision. Here are nine approaches ranked roughly from most passive to most hands-on.

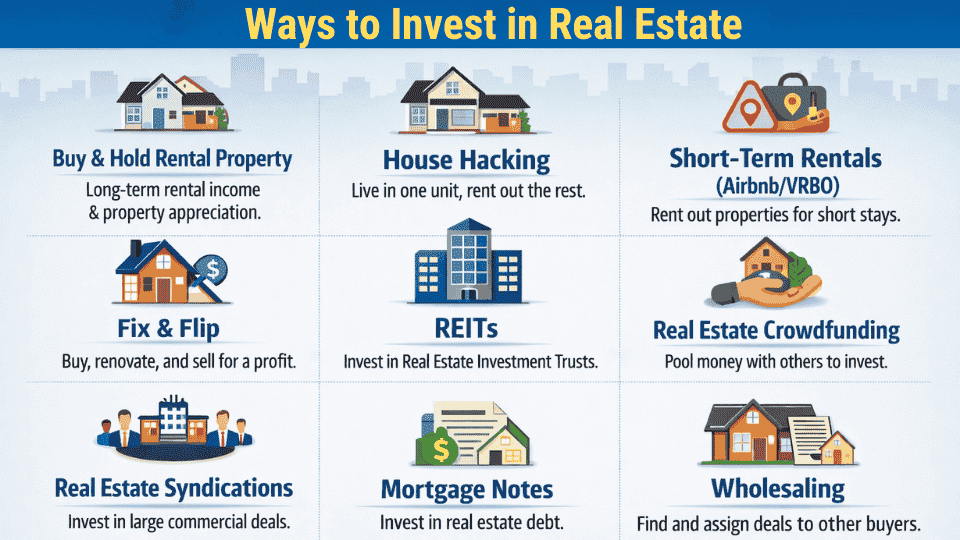

1. Buy and Hold Rental Property

Buy and hold is the classic real estate play, and for good reason. You purchase a property, rent it out, and collect monthly income while the property (ideally) grows in value. Over 10 or 20 years, your tenants are basically paying off your mortgage for you. That’s the wealth-building engine right there.

Pros

- Steady Cash Flow: Monthly rent checks create predictable income. In many US markets, a well-chosen rental can produce $200-$500/month in positive cash flow after expenses.

- Appreciation: US home values have historically risen 3-4% per year on average (according to Federal Housing Finance Agency data), though this varies significantly by market.

- Tax Benefits: You can deduct mortgage interest, property taxes, insurance, repairs, and depreciation, which often reduces your taxable rental income substantially.

- Equity Buildup: Every mortgage payment your tenant covers builds your ownership stake in the property.

Cons

- High Initial Investment: Expect to put down 20-25% on a non-owner-occupied investment property, plus closing costs (typically 2-5% of the purchase price) and a cash reserve for vacancies and repairs.

- Property Management: Dealing with tenant screening, midnight maintenance calls, and turnover costs real time and energy. Hiring a property manager typically runs 8-10% of gross rent.

- Market Fluctuations: Property values don’t always go up. The 2008 crash proved that, and localized downturns happen even in strong national markets.

- Illiquidity: Selling a property takes weeks or months. You can’t cash out overnight like you can with stocks.

2. House Hacking

House hacking is probably the best entry point for new investors, and it’s the strategy I recommend most often to people in their 20s and 30s. You buy a multi-unit property (duplex, triplex, or fourplex), live in one unit, and rent out the rest. The rental income offsets your mortgage, and because you’re living there, you qualify for owner-occupied financing with lower down payments.

Pros

- Lower Living Expenses: In many markets, renting out 2-3 units of a fourplex covers your entire mortgage. Some house hackers live for free or even cash-flow positive.

- Low Entry Cost: FHA loans require only 3.5% down on owner-occupied multi-family properties (up to 4 units). On a $300,000 property, that’s $10,500 versus $60,000+ for a traditional investment loan.

- Learning Experience: You get hands-on landlord experience with tenants right next door, which is a low-stakes way to learn property management.

- Rental Income: The extra income can go straight into savings for your next investment property.

Cons

- Less Privacy: Your tenants are your neighbors. If that idea stresses you out, this strategy may not be the best fit.

- Management Responsibility: You’re the landlord on-site. Tenants will knock on your door when the heater breaks.

- Limited Availability: Multi-family properties make up a smaller share of housing inventory in many suburban markets. You may need to look in urban areas or older neighborhoods.

- Scalability Limitations: You can only live in one property at a time. To grow, you’ll eventually need to move out and buy your next house hack or transition to traditional rentals.

3. Short-Term Rentals (Airbnb/VRBO)

Short-term rentals can generate significantly more income than traditional leases, sometimes 2-3x the monthly revenue in the right market. You buy a property, furnish it, and list it on platforms like Airbnb or VRBO. Guests book nightly or weekly stays, and you (or a co-host) handle turnover and guest communication.

The catch? Regulations have tightened across the US. Cities like New York, Los Angeles, and Nashville now restrict or heavily regulate short-term rentals. Always check local ordinances before buying.

Pros

- Higher Income Potential: A property that rents for $1,500/month as a long-term rental might gross $3,000-$4,500/month on Airbnb in a high-demand area.

- Flexibility: You can block off dates for personal use, making this attractive for vacation-area properties.

- No Long-Term Leases: If you get a problem guest, they’re gone in a few days, unlike a bad tenant locked into a 12-month lease.

- Strong Demand in Tourist Markets: Beach towns, mountain communities, and cities with year-round events tend to support strong STR occupancy.

Cons

- Time and Effort: Turnovers between guests require cleaning, restocking, and communication. Even with a co-host or management service (which typically takes 20-30% of revenue), it’s more work than a long-term rental.

- Regulatory Risks: Local governments are cracking down. A city that allows STRs today could ban them next year. Always verify zoning and permit requirements.

- Income Inconsistency: A ski cabin might sit empty from April through November. Seasonality is real, and your income won’t be steady month to month.

- Higher Operating Costs: Between cleaning fees, furnishing costs, platform fees (Airbnb takes ~3% from hosts), supplies, and higher wear and tear, your expenses run significantly higher than a traditional rental.

4. Fix and Flip

Flipping means buying a property below market value (usually one that needs work), renovating it, and selling it for a profit. It’s the most active real estate strategy on this list, and it’s not as easy as the TV shows make it look.

A common rule of thumb is the 70% rule: don’t pay more than 70% of the property’s after-repair value (ARV) minus renovation costs. So if a home will be worth $300,000 after renovation and repairs cost $50,000, your maximum purchase price is $160,000. That margin protects your profit if costs run over.

Pros

- Quick Profit Potential: A well-executed flip can net $30,000-$80,000 in profit over 3-6 months, though results vary wildly by market and project.

- Value Control: You directly influence the property’s value through your renovation choices, unlike most investments where you’re at the mercy of market forces.

- Skill Building: Flipping teaches you renovation, project management, and market analysis fast because your money is on the line.

- Scalability: Experienced flippers can run multiple projects simultaneously, building a repeatable business model.

Cons

- High Initial Investment: Between the purchase price, renovation budget, and carrying costs (mortgage, insurance, utilities during the project), you might have $150,000+ tied up in a single flip.

- Market Sensitivity: If the market softens while you’re mid-renovation, your projected profit can evaporate. Always build a 20-25% cost buffer into your budget.

- Cost Overruns: Contractors go over budget. Inspections reveal hidden damage. A project you budgeted at $40,000 can balloon to $60,000 fast.

- Time Pressure: Every month the property sits unsold, you’re paying the mortgage, insurance, and taxes with no income coming in.

5. Real Estate Investment Trusts (REITs)

If you want real estate exposure without touching a property, REITs are the simplest path. A REIT is a company that owns, operates, or finances income-producing properties like apartments, malls, warehouses, or office buildings.

By law, REITs must distribute at least 90% of their taxable income to shareholders as dividends. You buy shares through a brokerage account the same way you’d buy stock.

Pros

- Low Entry Cost: You can buy a single share of a REIT for under $50. ETFs like Vanguard Real Estate ETF (VNQ) give you exposure to dozens of REITs in one purchase.

- Diversification: A single REIT ETF might hold interests in apartment buildings, data centers, cell towers, and warehouses, spreading your risk across property types and geographies.

- Liquidity: Publicly traded REITs can be bought and sold during market hours, unlike physical property that takes months to sell.

- No Management: No tenants, no repairs, no 2am phone calls. The REIT’s management team handles everything.

Cons

- Stock Market Volatility: REITs trade on exchanges, which means they fluctuate with broader market sentiment. During the 2020 crash, some REITs dropped 40%+ before recovering.

- Limited Control: You have no say in which properties the REIT buys or sells. You’re trusting the management team’s judgment.

- Dividend Taxation: Most REIT dividends are taxed as ordinary income, not at the lower qualified dividend rate. Holding them in a tax-advantaged account (like an IRA) can help.

- Management Fees: Non-traded REITs, in particular, can carry high fees that eat into returns. Stick with publicly traded REITs if you’re starting out.

6. Real Estate Crowdfunding

Real estate crowdfunding platforms like Fundrise, CrowdStreet, and RealtyMogul let you pool money with other investors to fund real estate projects.

Some platforms are open to anyone with as little as $10, while others require you to be an accredited investor (meaning you earn $200,000+ annually or have a net worth above $1 million, excluding your primary home).

Pros:

- Low Minimum Investment: Fundrise lets you start with as little as $10. Other platforms may require $500-$1,000.

- Access to Larger Deals: Through pooling, you can participate in commercial developments and apartment complexes that would otherwise require hundreds of thousands of dollars.

- Diversification: Spread your money across multiple projects, property types, and geographic markets.

- Return Potential: Some platforms have historically reported annualized returns in the 8-12% range, though past performance doesn’t guarantee future results.

Cons:

- Illiquid: Your money is typically locked up for 3-7 years. Most platforms don’t offer easy early redemption.

- Platform Fees: Annual management fees of 1-2% are standard, plus potential performance fees that reduce your net return.

- Risk of Loss: These are real estate investments, not savings accounts. If a development project fails, you could lose part or all of your investment.

- Limited Transparency: Some platforms provide sparse project updates, making it hard to know how your investment is performing until distributions arrive.

7. Real Estate Syndications

Real estate syndications are group investments where a sponsor (also called the general partner or GP) finds, purchases, and manages a large property like an apartment complex or commercial building. You, as a limited partner (LP), invest capital and receive a share of the income and profits. You’re passive after writing the check.

Most syndications require you to be an accredited investor and have a minimum of $25,000-$100,000.

Pros

- Access to Large Deals: Syndications open the door to 100+ unit apartment buildings and commercial properties you’d never afford on your own.

- Passive Income: After your initial investment, you receive quarterly or monthly distributions without lifting a finger.

- Professional Management: Experienced sponsors handle acquisitions, renovations, tenant management, and eventual sale.

- Return Potential: Many syndications target 12-20% annualized returns (including appreciation), though these are projections, not guarantees.

Cons

- High Minimums: Most syndications require $25,000-$100,000 to participate, putting them out of reach for many beginners.

- Long Hold Periods: Typical syndication timelines are 5-7 years. Your capital is locked until the property is sold or refinanced.

- Sponsor Risk: A bad sponsor can tank an otherwise good deal. Thorough due diligence on the sponsor’s track record is non-negotiable.

- No Liquidity: You can’t sell your share on an exchange. If you need your money back early, you’re mostly out of luck.

8. Mortgage Notes and Debt Investing

Note investing flips the script. Instead of owning the property, you own the loan. When someone takes out a mortgage, that loan can be bought and sold. As the note holder, you collect interest payments from the borrower. The property serves as your collateral.

Notes come in two varieties: performing (borrower is making payments) and non-performing (borrower has stopped paying). Performing notes are lower risk and produce a steady income. Non-performing notes are cheaper to buy but require workout strategies, including potential foreclosure.

Pros

- Steady Income: Performing notes produce predictable monthly interest payments, similar to bond income.

- Collateral Protection: If the borrower defaults, you have a claim on the property as collateral.

- No Property Management: You’re not dealing with tenants, toilets, or trash. The borrower maintains the property.

Cons

- Default Risk: If the borrower stops paying, you may need to foreclose, which is costly and slow. In some US states, foreclosure takes over a year.

- Legal Complexity: Note investing requires understanding loan documents, state-specific foreclosure laws, and servicing regulations. It’s not beginner-friendly without guidance.

- Capped Returns: Your upside is limited to the interest rate on the note. You don’t benefit from property appreciation the way an owner would.

- Illiquidity: There’s no public market for mortgage notes. Selling one requires finding a buyer, which can take time.

9. Wholesaling

Wholesaling is the real estate equivalent of being a middleman. You find a property (usually distressed or undervalued), get it under contract at a below-market price, and then sell (or “assign”) that contract to another investor for a fee. You never actually buy the property.

Assignment fees typically range from $5,000 to $15,000 per deal, though they can go higher on larger transactions. Be aware that some states are tightening regulation of wholesaling, so check your local laws.

Pros

- Low Capital Required: You don’t need money to buy the property. Your only costs are marketing and earnest money deposits (often $500-$1,000).

- Fast Turnaround: Deals can close in 2-4 weeks, making this one of the quickest ways to generate cash in real estate.

- Network Building: Active wholesaling connects you with buyers, sellers, agents, and investors, building a valuable network for future deals.

Cons

- Time-Intensive: Wholesaling is a hustle, not a passive investment. You’re constantly marketing for leads, negotiating with sellers, and finding buyers.

- Legal Risks: Assignment contracts must be airtight. In some states, wholesaling without a real estate license is a legal gray area. Consult an attorney before your first deal.

- Inconsistent Income: Some months you close three deals; other months, zero. There’s no guaranteed paycheck.

- No Ownership: You don’t build equity, collect rent, or benefit from appreciation. Once the deal closes, you’re back to hunting for the next one.

What Are the Tax Benefits of Real Estate Investing?

One of the biggest advantages of real estate over other investments is the tax treatment. Here’s what US investors can typically deduct or benefit from:

Depreciation is the IRS’s way of acknowledging that buildings wear out over time. For residential rental property, you can depreciate the building’s value (not the land) over 27.5 years, creating a paper loss that offsets your rental income even when the property is actually making money. This is one of the most powerful tax benefits in real estate.

Mortgage interest and operating expenses like property taxes, insurance, repairs, property management fees, and travel to your rental property are generally deductible against rental income.

1031 exchanges let you defer capital gains taxes when you sell an investment property by reinvesting the proceeds into another qualifying property within a specific timeline (45 days to identify, 180 days to close). This allows you to keep growing your portfolio without a tax hit on every sale.

Pass-through deduction under IRS Section 199A may allow qualifying real estate investors to deduct up to 20% of their net rental income before calculating their tax bill.

Tax laws are complex and change frequently. The information above is general in nature. Consult a CPA or tax professional who specializes in real estate to understand how these benefits apply to your specific situation.

Is Real Estate a Better Investment Than Stocks?

This comes up constantly, and the honest answer is: it depends on what you’re optimizing for.

Stocks (particularly index funds like the S&P 500) have historically returned about 10% annually before inflation. They’re liquid, require zero maintenance, and you can start with virtually any dollar amount.

Real estate typically appreciates at 3-4% per year, but that’s not the full picture. When you factor in leverage (using a mortgage to control a $300,000 asset with $60,000 down), rental income, tax benefits, and equity buildup, the total return on your invested cash can significantly outpace stocks.

The practical difference? Stocks give you simplicity and liquidity. Real estate gives you leverage, cash flow, and tax advantages, but demands more capital, knowledge, and involvement. Most financial advisors suggest holding both for a well-diversified portfolio.

What Is the Difference Between Active and Passive Real Estate Investing?

Active investing means you’re directly involved in finding, buying, managing, or renovating properties. Rental property ownership, house hacking, flipping, and wholesaling all fall into this bucket. You control the decisions, but you’re also putting in time and energy.

Passive investing means your money works while you don’t. REITs, crowdfunding, syndications, and note investing are passive strategies where professionals manage the assets, and you collect returns.

Neither approach is universally better. Active investing typically offers higher returns and more control but demands more time. Passive investing is hands-off but comes with less control and sometimes lower returns. Many experienced investors use both active properties for wealth building and passive investments for diversification.

How Much Money Do You Need to Start Investing in Real Estate?

The amount you need depends entirely on your chosen strategy. Here’s a realistic breakdown:

Under $500: REITs and crowdfunding platforms like Fundrise let you invest with as little as $10-$500. You won’t get rich fast, but you’ll gain exposure to real estate returns and learn how the asset class behaves.

$10,000-$25,000: House hacking with an FHA loan (3.5% down) on a $250,000-$400,000 multi-family property is achievable in this range, including closing costs and initial reserves. This is where many first-time investors start.

$50,000-$100,000: Traditional rental property purchases (20% down) in affordable US markets like the Midwest and Southeast, or entry into real estate syndications.

$100,000+: Fix-and-flip projects, multiple rental properties, or commercial real estate. At this level, you’re building a portfolio, not buying a single asset.

The right move is to start wherever you are right now and build from there. Plenty of successful real estate investors began with a $500 REIT investment or a house hack with an FHA loan.

How Do You Choose the Right Real Estate Investing Strategy?

Choosing a strategy comes down to five honest questions:

How much capital do you have right now? If you’re working with under $1,000, start with REITs or crowdfunding. If you’ve saved $15,000-$25,000, house hacking is likely your best first move. More than $50,000 opens the door to direct property ownership or syndications.

How much time can you commit? If you work full-time and don’t want a second job, stick with passive options like REITs, crowdfunding, or syndications. If you have evenings and weekends to spare, rental properties or house hacking are viable.

How much risk can you stomach? Flipping carries the highest short-term risk. Buy-and-hold rentals are moderate risk over the long term. REITs carry market volatility but low overall risk to your capital.

Do you want to be hands-on or hands-off? There’s no wrong answer here. Some people love the control of managing their own properties. Others want to invest and forget about it.

What’s your timeline? If you need returns within months, flipping or wholesaling might work. If you’re building wealth over 10-20 years, buy-and-hold or REIT investing aligns better.

Step-by-Step How to Start Investing Today?

Step 1: Get clear on your “why.” Are you looking for monthly cash flow to supplement your income? Long-term wealth accumulation for retirement? A specific dollar amount within a specific timeline? Write it down. Vague goals lead to indecisive action.

Step 2: Get your finances in order. Before investing a dollar in real estate, have at least 3-6 months of living expenses saved in an emergency fund. Check your credit score (aim for 680+ for most investment loans, 580+ for FHA). Pay down high-interest debt first.

Step 3: Pick your strategy. Use the decision framework above. Match your budget, timeline, and involvement preference to a strategy. Don’t try to do everything at once.

Step 4: Research your market. If you’re buying property, study local rental rates, vacancy rates, median home prices, and employment trends. Tools like Zillow, Redfin, and Rentometer can help. If you’re investing in REITs or crowdfunding, research platform track records and fee structures.

Step 5: Run the numbers. For rental properties, calculate your expected cash-on-cash return, cap rate, and monthly cash flow. For passive investments, compare historical returns and fee structures. Never invest based on gut feeling alone.

Step 6: Make your first investment. Start small. Buy one share of a REIT. Put $500 into a crowdfunding platform. Make an offer on a duplex. The first deal is the hardest because everything after it gets easier.

Step 7: Reinvest and scale. Once you’ve got one investment under your belt, use the income and experience to fund the next one. Many successful portfolios started with a single property or a small REIT allocation and grew over 5-10 years.

Common Mistakes to Avoid When Investing in Real Estate

Learning from common errors can save you money and stress. Here are mistakes many new investors make and how to avoid them.

| Mistake | Why It Causes Problems | Better Approach |

|---|---|---|

| Taking on too much debt | Creates pressure and financial strain | Borrow within safe limits |

| Skipping market research | Leads to poor decisions | Study trends and rental demand |

| Misjudging costs | Cuts into earnings | Plan for repairs and surprises |

| Buying based on emotion | Can lead to weak decisions | Focus on numbers and facts |

| Not spreading investments | Raises risk | Mix different real estate options |

How to Reduce Risk in Real Estate Investing?

Risk is part of real estate investing. You can’t eliminate it, but you can manage it.

Build cash reserves: Keep at least 6 months of mortgage payments, taxes, and insurance per property in a dedicated savings account. This covers you during vacancies, unexpected repairs, or market dips.

Diversify your approach: Don’t put all your capital into a single property in a single market. Combining direct ownership with passive investments, such as REITs, spreads your risk across property types and geographies.

Use conservative financing: Aim for a loan-to-value ratio of 75-80%. The more equity you have in a property, the better positioned you are to weather a downturn.

Get professional help: Build relationships with a real estate attorney, a CPA who understands investment property taxation, and an experienced property manager. The cost of professional advice is almost always less than the cost of learning expensive lessons on your own.

I’ve worked with investors who lost significant money simply because they didn’t have a real estate attorney review their purchase contract. One client discovered a lien on a property that would have cost $45,000 to resolve, and they found it only because we insisted on a thorough title search. That $500 in legal fees saved them from a disaster.

Summing It Up

Real estate investing offers real opportunities to build wealth over time. Whether you choose to buy rental property, try house hacking, or invest through REITs, the key is starting with a method that fits your budget and goals.

Take time to study your options and be honest about what you can afford and manage. Start small if needed. Many successful investors began with just a few hundred dollars in REITs or a single rental property.

What matters most is taking that first step and learning as you go. Avoid common mistakes by doing your research, keeping reserve funds, and seeking advice when needed.

Your financial future can include real estate. Choose your path, stay patient, and watch your investments grow.