You’ve landed £100,000. Maybe it came from an inheritance, the sale of a property, or years of careful saving.

The instinct is to act fast, but Martin Lewis says to slow down and plan first.

The Martin Lewis best way to invest 100k isn’t about picking the hottest fund or chasing the best rate on the market this week.

It starts with a checklist that protects your money before investing.

This blog walks through how to invest 100k in that exact order, fills in the gaps other guides skip, and shows you where the real decisions get complicated.

This article is for informational purposes only and does not constitute regulated financial advice. For advice tailored to your circumstances, speak to an FCA-authorised independent financial adviser.

Who Is Martin Lewis?

Martin Lewis founded MoneySavingExpert.com in 2003 with £100. He later sold it to MoneySuperMarket for £87 million but kept editorial independence as a contractual condition of the sale.

He was awarded an OBE in 2014 for services to consumer rights and financial education.

What sets him apart from most voices in personal finance is that he doesn’t sell financial products. His guidance is based on publicly available information, independent research, and a consumer-first approach.

He’s also consistent about one thing: he’s not a regulated financial adviser, and he says so openly.

His investment framework isn’t original in any academic sense; it draws on well-established principles like tax efficiency, diversification, and compound growth.

What he does well is translate those principles into plain steps that people can actually follow.

Martin Lewis’s Core Rules for a £100k Investor

These five rules appear consistently across Martin Lewis’s published guidance on MoneySavingExpert.com:

| Rule | What It Means |

|---|---|

| Invest for at Least Five Years | Only invest money you won’t need in the short term, as markets can fluctuate. |

| Keep Costs Low | Choose low-cost index funds rather than expensive actively managed funds. |

| Stay Invested | Avoid panic-selling during market downturns. Long-term investing typically delivers better results. |

| Protect Large Cash Balances | Don’t keep more than £85,000 with a single banking license to maintain FSCS protection. |

| Review Annually | Check your portfolio once a year and avoid constantly monitoring or making frequent changes. |

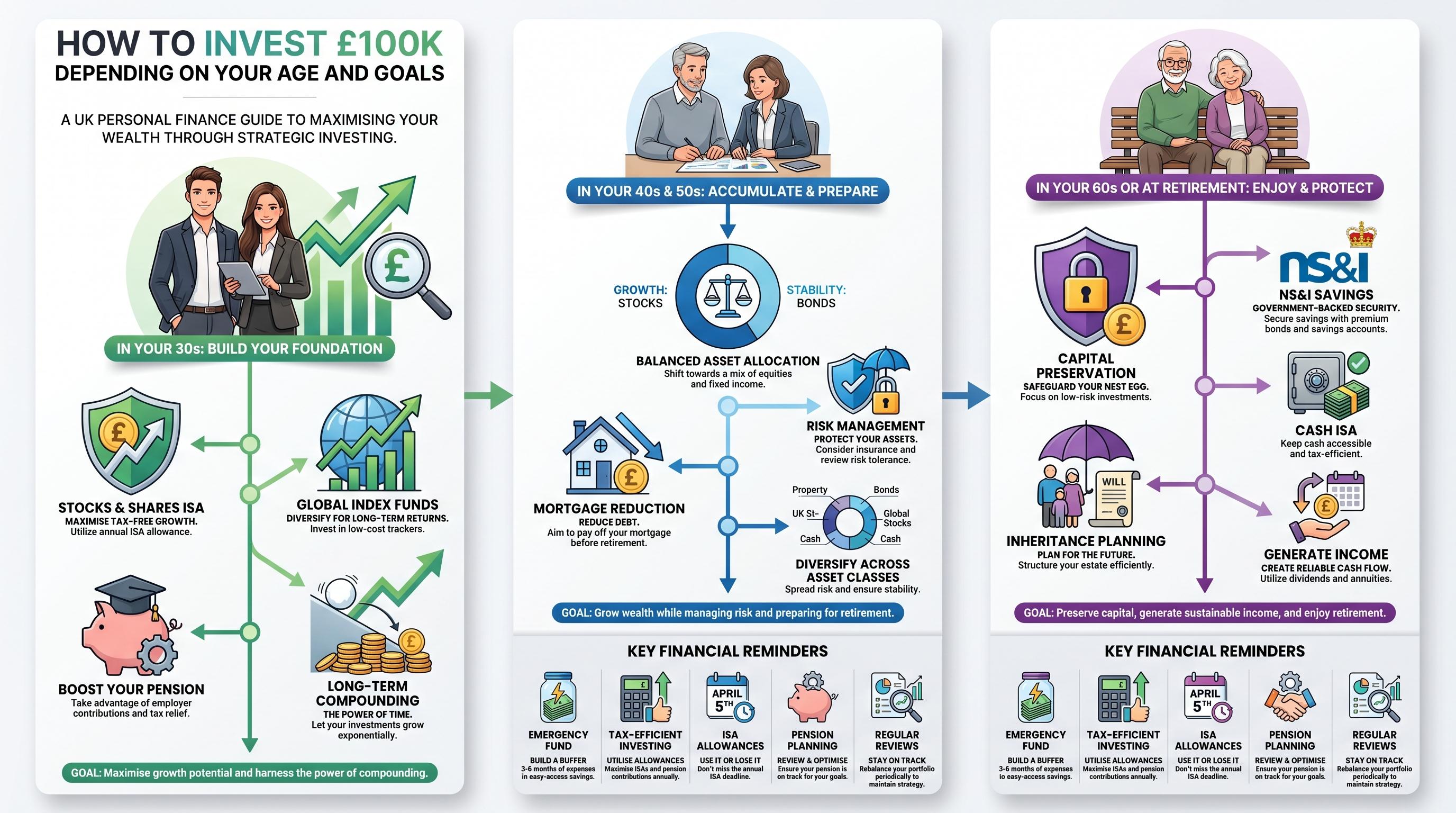

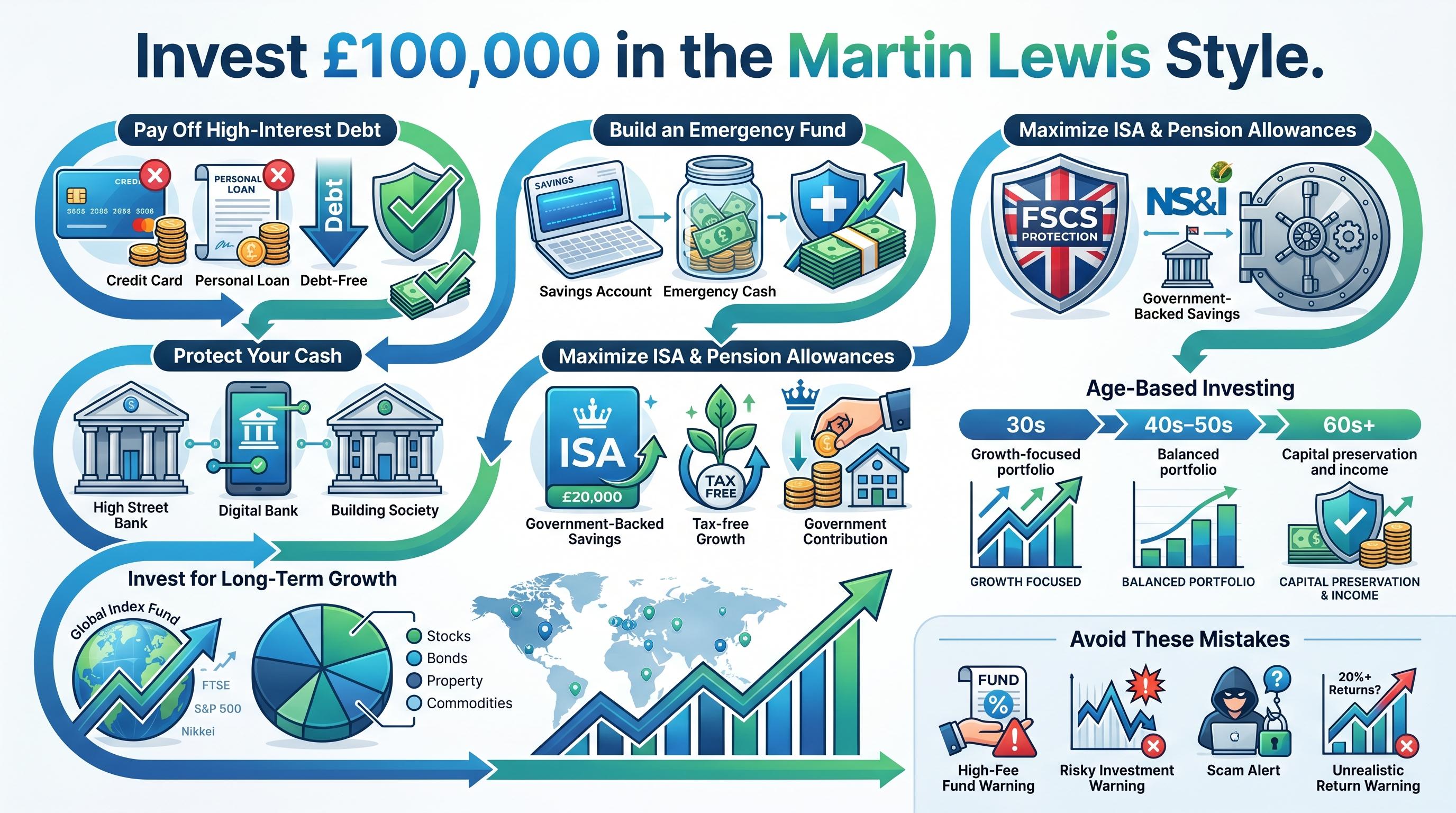

Age-Based Strategies for Investing £100,000

Most guides on this topic skip age-based advice entirely, even though it can change the whole plan. The right split between growth assets and safer options depends heavily on your time horizon.

- In Your 30s: 30+ years until retirement means you can handle market ups and downs. Focus on maximizing contributions to a Stocks and Shares ISA and pension, invest in low-cost global index funds, and stay invested for the long term.

- In Your 40s and 50s: Retirement is approaching, so a balance between growth and stability becomes more important. Consider a mix of equities and fixed-income investments, and review whether mortgage overpayments should take priority, particularly if you’re on a mortgage rate close to 7% rather than one of the cheap fixed deals from a few years ago.

- In Your 60s or at Retirement: Capital preservation becomes the main goal. Consider NS&I products, Cash ISAs, and short-term fixed savings accounts for money needed in the near future. Also review inheritance tax planning, especially with upcoming pension rule changes.

Best Way to Invest £100,000 in the Martin Lewis Style

Investing £100,000 starts long before buying funds or shares. Martin Lewis stresses that the smartest first moves involve strengthening your financial position, reducing risk, and making the most of tax advantages.

Step 1: Clear High-Interest Debt First

Before a single pound goes into an ISA or pension, Martin Lewis’s position is firm: pay off high-interest debt.

The logic is straightforward. If you’re carrying a credit card balance at 20% interest and your investment is returning 7%, you’re losing 13% on that money.

No investment reliably beats the guaranteed return of clearing expensive debt.

What about your mortgage or student loan? Those get more complicated. A student loan on Plan 2 charges up to 6.9% interest, making it worth considering whether to clear it.

A 2.5% mortgage probably doesn’t need to be the first priority. More on mortgage decisions below.

Step 2: Set Aside an Emergency Fund

You should not invest your full £100,000. Martin Lewis consistently recommends keeping three to six months of essential living costs in an easy-access savings account before investing in long-term investments.

The reason matters: if your boiler breaks or you lose your job, you need cash you can reach without selling investments at the wrong moment.

Markets go down. If you’re forced to sell during a dip because you have no liquid savings, a short-term emergency becomes a long-term financial loss.

Where to keep this fund? A top-paying easy-access account, spread across institutions to stay within the £85,000 FSCS limit.

Step 3: Understand the £85,000 FSCS Rule

The Financial Services Compensation Scheme protects up to £85,000 per banking license if a bank fails. At £100,000, you’re above that threshold, which makes account placement a real decision rather than an afterthought.

A common mistake is assuming that “per bank” and “per banking license” mean the same thing. They don’t. HSBC and First Direct share a single banking license. Lloyds, Halifax, and Bank of Scotland also share one.

Putting £50,000 in each of those two groups gives you £100,000 across four brand names, but only £85,000 of it is protected per group.

The practical fix: split your cash across institutions that hold separate licenses.

Alternatively, NS&I (National Savings & Investments) is backed directly by the UK government and has no £85,000 cap. It’s not the highest rate on the market, but the protection is complete.

Step 4: Use Your Tax Wrappers Before Anything Else

This is where the investing actually starts. The two main wrappers in the UK are Stocks and Shares ISAs and pensions (including SIPPs). Both shelter your returns from tax. The difference is access.

Stocks and Shares ISA

An ISA is the simplest tax shelter available for £100,000, but the annual limit means it takes a few years to move the full amount in.

- ISA Allowance: You can invest up to £20,000 per tax year in an ISA, with all growth, dividends, and interest free from income tax and capital gains tax.

- For £100,000: The £20,000 can be sheltered in an ISA this tax year. The remaining money will need to be held elsewhere initially.

- Use a Bed and ISA: Invest excess funds in a General Investment Account (GIA) now, then transfer up to the annual ISA allowance each new tax year to gradually move investments into a tax-free wrapper.

- 2026/27 Opportunity: With the Cash ISA allowance expected to fall from £20,000 to £12,000 in April 2027, making full use of the current £20,000 allowance before the change could be worthwhile.

Pension / SIPP

A pension gives you tax relief on the way in, but the money is locked away until at least your late 50s, so it works best for cash you won’t touch for decades.

- Tax Relief: Pension contributions receive income tax relief. For example, an £800 contribution becomes £1,000 for basic-rate taxpayers, while higher-rate taxpayers can reduce the effective cost of a £1,000 contribution to around £600.

- Annual Allowance: You can contribute up to £60,000 per year (or 100% of earnings, if lower) in 2025/26.

- Access Restrictions: Pension funds are generally inaccessible until age 57 from 2028, making them less suitable if you may need the money sooner.

- Inheritance Tax Change: From April 2027, pension pots are expected to be included in an estate for inheritance tax purposes, potentially affecting long-term estate planning decisions.

Where Does the Remaining £80,000 Go?

The short version: fixed-rate bonds, NS&I Premium Bonds, or a General Investment Account, depending on how soon you need the money.

Since you can only put £20,000 into an ISA each tax year, the rest needs somewhere to sit while you transfer it. Here’s how to think about it:

- Fixed-Rate Savings Bonds: Lock in a guaranteed return for 1–2 years, stay within FSCS protection limits, and review options when the term ends. Suitable for those seeking certainty without market risk.

- NS&I Premium Bonds: Hold up to £50,000 with tax-free prizes. They can be especially attractive for higher-rate taxpayers who have used their Personal Savings Allowance.

- General Investment Account (GIA): A practical home for money waiting to be moved into an ISA. Low-cost global index funds can provide long-term growth, while the Bed and ISA strategy gradually reduces future tax exposure.

- What Martin Lewis Typically Avoids: High-fee actively managed funds, large allocations to peer-to-peer lending, and investments promising unusually high returns.

What If You Inherited the £100k?

| Consideration | Why It Matters | Action to Take |

|---|---|---|

| Don’t Invest Immediately | Large financial decisions made during grief can lead to regrets later. | Take a few months before making major investment choices. |

| Check Inheritance Tax Status | Inheritance tax is usually settled by the estate, but it’s important to confirm. | Verify with the solicitor or executor handling the estate. |

| Watch for Investment Scams | Bereavement can make people targets for fraudsters and unsolicited advisers. | Be cautious of unexpected investment offers and seek regulated advice if needed. |

If your £100,000 comes from an inheritance rather than years of saving, the approach should be slightly different.

If part of it came from selling an inherited house, it’s worth checking whether stamp duty on inherited property applies before you decide what to do with the proceeds.

Before making any investment decisions, take time to understand the tax position, review your financial goals, and avoid rushing into choices.

Which Investments Does Martin Lewis Recommend?

He doesn’t recommend specific products. He points people toward broad categories instead: low-cost index funds, bonds, and cautious diversification across asset types.

His advice often highlights choosing options based on your goals, risk tolerance, fees, and personal circumstances.

- Low-cost global index funds and ETFs: One of his most consistently repeated recommendations is investing in low-cost, diversified funds that track global markets rather than trying to pick individual winners.

- Bonds and gilts for stability: He often highlights bonds and government-backed investments as lower-risk options with more predictable returns.

- Property investments: Martin Lewis discusses property, including buy-to-let and REITs, while warning investors to consider costs, taxes, maintenance, and the fact that property is less liquid than many other investments.

- Peer-to-peer lending (P2P) caution: He has warned about the risks of P2P lending, including the lack of FSCS protection and the risk of borrower default.

- Cryptocurrency caution: Lewis has described cryptocurrency as closer to gambling than to traditional investing due to its volatility and uncertainty. He advises people to understand the risks before investing money.

Conclusion

The Martin Lewis approach to investing 100k in the UK won’t win any prizes for excitement.

Clear the debt, build the buffer, protect your cash from the FSCS gap, fill the ISA, top up the pension, and put the rest in low-cost index funds. Do it in that order.

What makes it worth following isn’t novelty; it’s the fact that these steps, taken in sequence, remove most of the ways people accidentally lose money when they have a large sum to invest.

The order matters as much as the individual choices.

If your situation is more complex, a larger portfolio, property investment, inheritance tax planning, or early retirement, a one-off session with a regulated IFA is money well spent

Frequently Asked Questions

How Much Does a One-Off Financial Adviser Session Cost?

Fixed-fee one-off advice from an IFA typically starts around £500, rising to £1,000 or more for full financial planning.

How Much Interest Will 100K Earn in a Year?

If £100,000 is in a savings account paying 5% AER, it would earn about £5,000 in interest over one year before any applicable tax.

Can I Live Off the Interest of 100K?

No, not usually. At typical savings rates of 3%–5%, £100,000 would generate about £3,000–£5,000 per year (£250–£417 per month), which is unlikely to cover most living expenses.