Semi-commercial properties combine residential and commercial spaces in one building, such as apartments above shops or homes with attached offices.

Financing these properties can be more complex than standard mortgages. Residential lenders often focus on personal income and occupancy, while commercial lenders prioritize lease strength and business risk.

Semi-commercial mortgages are designed for mixed-use buildings. They assess both residential rental income and commercial lease revenue together, giving lenders a clearer view of the property’s total earning potential.

This guide covers how semi-commercial mortgages work, the main types available, eligibility criteria, and the pros and cons of semi-commercial financing compared to residential or commercial financing.

What are Semi-Commercial Mortgages?

Semi-commercial mortgages finance properties where residential and commercial spaces coexist.

Unlike purely residential mortgages, which evaluate only owner-occupied status, or commercial mortgages, which assess only business revenue, semi-commercial mortgages evaluate both.

Lenders assess the property’s total income potential, including rental income from residential units combined with commercial lease revenue.

This dual-income approach allows borrowers to qualify based on the property’s actual cash flow rather than on personal income or employment status alone.

- Semi-commercial properties present a complexity that conventional lenders struggle to address. A standard residential lender lacks underwriting guidelines for retail components.

- A commercial lender focuses solely on business operations and ignores residential value. Semi-commercial, specialized lenders bridge this gap by evaluating the complete property picture.

Semi-commercial mortgages finance properties where residential and commercial spaces coexist. The fundamentals differ significantly from residential or purely commercial products.

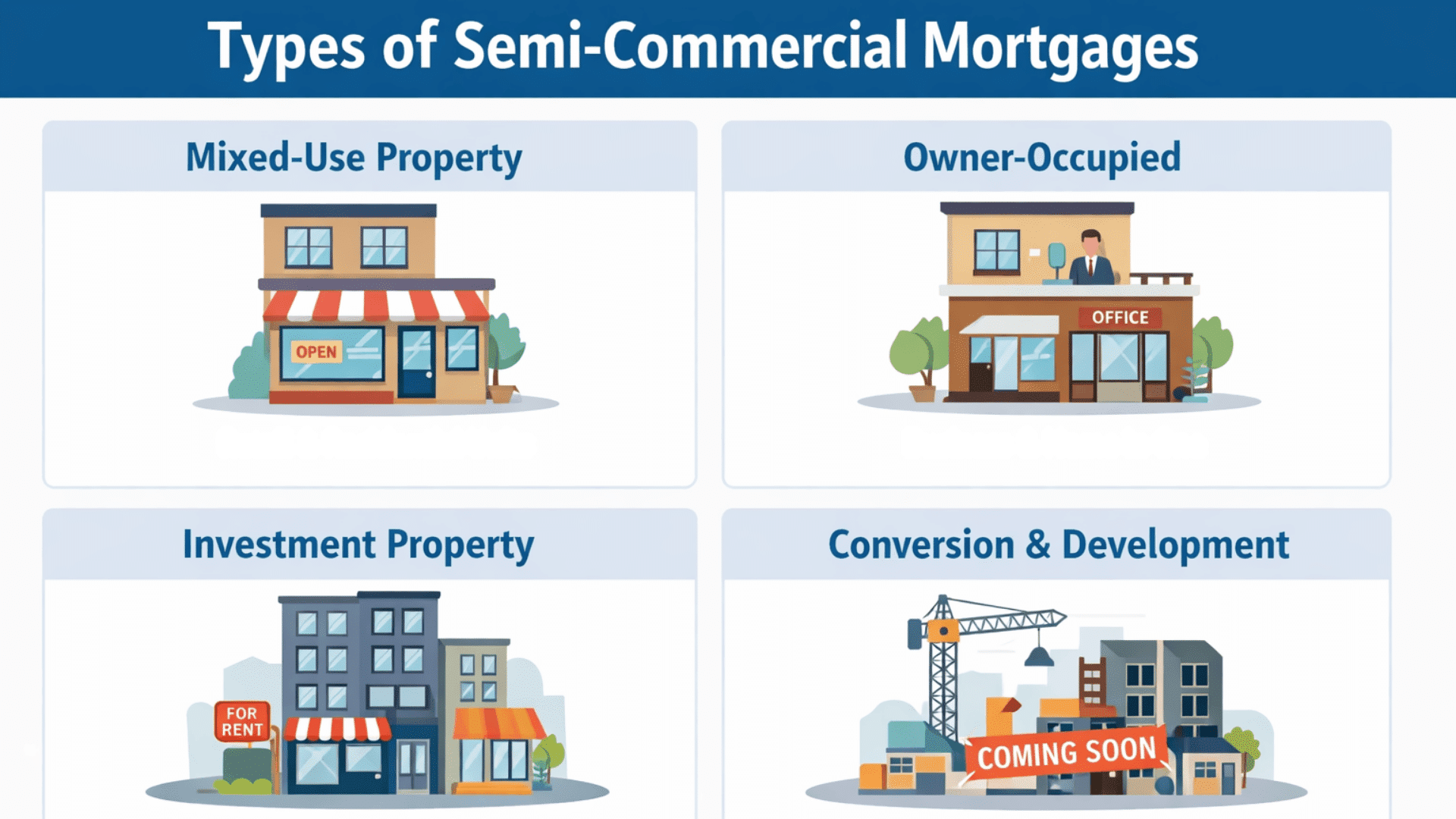

Types of Semi-Commercial Mortgages

Semi-commercial mortgages vary based on property composition and financing structure. Understanding these categories helps you identify which product matches your property situation.

1. Mixed-Use Property Mortgages

Properties financed: Buildings combining residential units with ground-floor retail, restaurants, offices, or service businesses.

How they work: Lenders evaluate residential rental income plus commercial lease revenue. Both income streams count toward qualifying and debt service calculations.

Rate range: 5.5%-7.5% (between residential and commercial rates).

Loan terms: 20-30 years are typical.

2. Owner-Occupied Commercial Properties with Residential

Properties financed: Business owner living in the same building (owner upstairs, office downstairs).

How they work: Primary focus on owner occupancy with secondary residential or commercial income factored into qualification.

Rate range: 5.0%-6.5% (closer to residential due to owner occupancy).

Loan terms: 15-30 years.

3. Investment Semi-Commercial Properties

Properties financed: Multi-unit buildings with business operations held as investment (not owner-occupied).

How they work: Lenders evaluate investment income from all sources, residential rent plus commercial lease revenue, as the primary qualifying factor.

Rate range: 6.0%-8.0% (closer to commercial due to investment focus).

Loan terms: 20-30 years.

4. Conversion and Development Semi-Commercial

Properties financed: Properties being converted from single-use to mixed-use or newly developed as semi-commercial.

How they work: Lenders evaluate projected income after conversion or development completion, using market rent assumptions.

Rate range: 6.5%-8.5% (higher due to development risk).

Loan terms: Construction phase plus 25-year amortization.

Semi-Commercial vs Residential vs Commercial Mortgages

Choosing the right mortgage type depends on your property type and income.

| Feature | Residential | Semi-Commercial | Commercial |

|---|---|---|---|

| Property Type | Homes, 1-4 units | Mixed-use buildings | Business properties only |

| Interest Rates | 3.5%-5.5% | 5.5%-7.5% | 7%-9%+ |

| Down Payment | 3%-20% | 10%-25% | 20%-30% |

| Qualification | Personal income | Combined property income | Property cash flow (DSCR) |

| Loan Terms | 15-30 years | 15-30 years | 5-25 years |

Semi-commercial mortgages offer a middle ground, combining the longer terms and accessibility of residential financing with the income-based qualification of commercial loans.

Eligibility Criteria for Semi-Commercial Mortgages

Semi-commercial qualification differs from purely residential or commercial financing, requiring evaluation of both income sources and property components. Here are the primary eligibility factors lenders assess.

| Eligibility Factor | Requirements |

|---|---|

| Credit Score | Minimum 620-640; 700+ receives better rates |

| Property Type | Many lenders require the property to be primarily residential, but acceptable commercial-to-residential ratios vary by lender. |

| Debt-to-Income Ratio | 40-50%, depending on property income stability |

| Down Payment | 15-25% for investment; 10-20% for owner-occupied |

| Commercial Tenant Stability | Active leases with established tenants; longer terms reduce risk |

| Residential Occupancy Rate | 80%+ occupancy or stable rental history required |

Meeting these eligibility criteria positions you to move forward with the actual application and documentation process.

How to Qualify for Semi-Commercial Mortgages

Qualifying for semi-commercial mortgages requires proving both residential rental income and commercial lease revenue. Lenders evaluate your property’s combined cash flow to determine borrowing capacity and approval odds.

Documentation Requirements

Once you meet the basic eligibility criteria, lenders require specific documents to prove both income streams and property performance.

- Residential income proof – Submit 12-24 months of bank statements showing rental deposits plus signed lease agreements with current tenants.

- Commercial income records – Provide 2 years of tax returns, profit-and-loss statements, and active commercial lease agreements with tenants.

- Property appraisals: Include professional appraisals that value both residential and commercial components separately and combined.

- Occupancy verification: Demonstrate an80%+ residential occupancy rate and active commercial tenant leases with remaining terms.

- Cash flow calculation – Lenders add residential and commercial income, subtract operating expenses, and verify the property covers loan payments.

Lenders use conservative income assumptions and factor in vacancy rates. Incomplete documentation significantly delays the underwriting process.

What Fees Are Charged on Semi-Commercial Mortgages?

Semi-commercial mortgages often carry fees that exceed those of typical residential mortgages because of the complexity of evaluating mixed-use properties.

Upfront Fees:

- Origination fees: 1%-2% of loan amount (covers underwriting and processing)

- Appraisal fees: $2,000-$5,000 (requires separate residential and commercial valuations)

- Application fees: $500-$1,500 (non-refundable)

- Due diligence costs: $1,000-$3,000 (environmental reports, property inspections)

- Attorney fees: $1,500-$3,500 (title review, closing documents)

Ongoing Fees:

- Annual fees: Some lenders charge 0.25%-0.5% annually for loan servicing

- Property management costs: 8%-12% of rental income if using third-party management

- Insurance premiums: Higher than residential due to commercial liability coverage

Exit Fees:

- Prepayment penalties: 1%-5% of the remaining balance if paying off early

- Yield maintenance: Compensates lender for lost interest (common on commercial-style terms)

- Defeasance costs: $10,000-$50,000+ for large loans with strict prepayment restrictions

Budget 3%-5% of your loan amount for total closing costs on semi-commercial mortgages, compared to 2%-3% on residential loans.

Pros and Cons of Semi-Commercial Mortgages

Semi-commercial financing offers distinct advantages and tradeoffs compared to residential or pure commercial mortgages.

This table outlines key considerations for evaluating whether semi-commercial financing aligns with your property needs.

| Advantages | Disadvantages |

|---|---|

| Lower rates than pure commercial (5.5%-7.5% vs. 7%-9%+) | Higher rates than residential (5.5%-7.5% vs. 3.5%-5.5%) |

| Combined income qualification increases borrowing capacity | Complex documentation requires both income stream proofs |

| DSCR requirements vary, but lenders typically want the property income to comfortably cover loan repayments. | Fewer lenders available limit rate shopping options |

| Property appreciation from income diversity | Market risk exposure from commercial downturns |

| Refinancing flexibility as property stabilizes | Prepayment restrictions and yield maintenance clauses |

| Higher loan amounts than residential-only properties | Lower borrowing capacity than pure commercial financing |

These errors directly impact your approval odds and final mortgage terms. Knowing what to avoid strengthens your application.

Common Mistakes Borrowers Make

Knowing common pitfalls helps you navigate the semi-commercial financing process more effectively and avoid costly decisions.

1. Overestimating Commercial Income – Projecting rental rates above market or occupancy higher than realistic. Lenders use conservative assumptions; verify with comparable properties.

2. Ignoring Tenant Quality – Weak tenants or short leases reduce property value. In the long term, creditworthy tenants improve mortgage terms and rates.

3. Underestimating Operating Expenses – Property taxes, insurance, maintenance, and vacancy rates reduce net income. Lenders deduct typical expenses from gross revenue.

4. Mixing Personal and Business Income – Failing to separate personal W-2 income from property-generated income complicates qualification. Document each income source clearly.

5. Neglecting Property Condition – Mixed-use properties require professional maintenance. Deferred maintenance reduces property value and lender confidence.

6. Accepting First Offer – Rates vary across lenders. Always compare at least 3 quotes for semi-commercial financing.

Final Thoughts

Semi-commercial mortgages provide a practical financing option for properties that combine residential and commercial uses.

While they involve more detailed underwriting than standard residential loans, they allow lenders to assess the full income potential of mixed-use buildings.

By considering both residential rental income and commercial lease revenue, these mortgages can offer greater borrowing flexibility than residential financing alone, often at lower costs than fully commercial loans.

Success depends on understanding your property’s structure, tenant stability, and income profile. Clear documentation and realistic income expectations are essential.

For investors and owner-occupiers dealing with mixed-use properties, semi-commercial mortgages can bridge the gap where traditional residential or commercial lending falls short.