Your home is probably your biggest financial asset, and at some point, you may need to access what you have built up in it. But the ways to get equity from a house are not all equal in cost, flexibility, or risk.

Some options leave your existing mortgage untouched. Others replace it entirely. A few are only suitable once you reach a certain age.

Choosing the wrong one based on incomplete information can cost you thousands, or worse, put your ownership at risk.

This guide breaks down every main route, including remortgaging, further advances, HELOCs, cash-out refinancing, equity release, and downsizing, so you can compare them properly before speaking to a broker.

What Home Equity Actually Means

Home equity is the portion of your property you own outright. You calculate it by subtracting your outstanding mortgage balance from the current market value of your home.

If your home is worth $400,000 and you still owe $220,000 on your mortgage, your equity stands at $180,000.

Why the Number Changes Over Time

That figure is not static. It grows as you pay down your mortgage principal, and it rises or falls alongside property values.

Even modest monthly overpayments can speed up equity growth over time.

The more equity you hold, the more options you have, and generally, the better the terms a lender will offer when you choose to access it.

Before making any decisions, get an accurate property valuation.

Equity estimates based on outdated figures can lead you to apply for the wrong product or attempt to borrow more than your lender will approve.

Remortgaging to Release Equity

Remortgaging means switching your existing mortgage to a new deal, often with a different lender.

When you remortgage for a larger amount than your outstanding balance, the surplus is released to you as a lump sum.

If you owe $150,000 on a home worth $300,000 and remortgage for $200,000, you access $50,000 in cash while the new mortgage replaces the old one.

Because your home serves as collateral, the interest rates available are typically far lower than those for personal loans or credit cards.

The released funds can be used for almost any purpose.

Cash-Out Refinancing: What It Is and When It Makes Sense

Cash-out refinancing is a close relative of remortgaging but worth understanding as its own option, particularly for homeowners comparing US-market products.

You take out a new mortgage for more than your current balance, pay off the old one, and pocket the difference.

The key trade-off is rate. If your current mortgage has a historically low rate, replacing it with a new loan at a higher rate will increase your monthly payments even if you access useful cash.

Run the full-term cost comparison, not just the monthly figure, before deciding whether this route makes sense for you.

Cash-out refinancing tends to work best when interest rates have fallen since you took out your original mortgage, or when you need a large lump sum, and the rate difference is small enough to absorb.

Further Advance from Your Existing Lender

A further advance is an additional loan from your current mortgage lender, secured against the same property.

Rather than replacing your existing mortgage, it sits alongside it as a separate facility that you repay in addition to your usual monthly payments.

Because you are not switching lenders, there are no solicitor transfer fees and no early repayment penalty on your current deal.

The application process is quicker and simpler than a full remortgage.

This makes it one of the more cost-efficient options when you need equity access without disrupting a deal worth keeping.

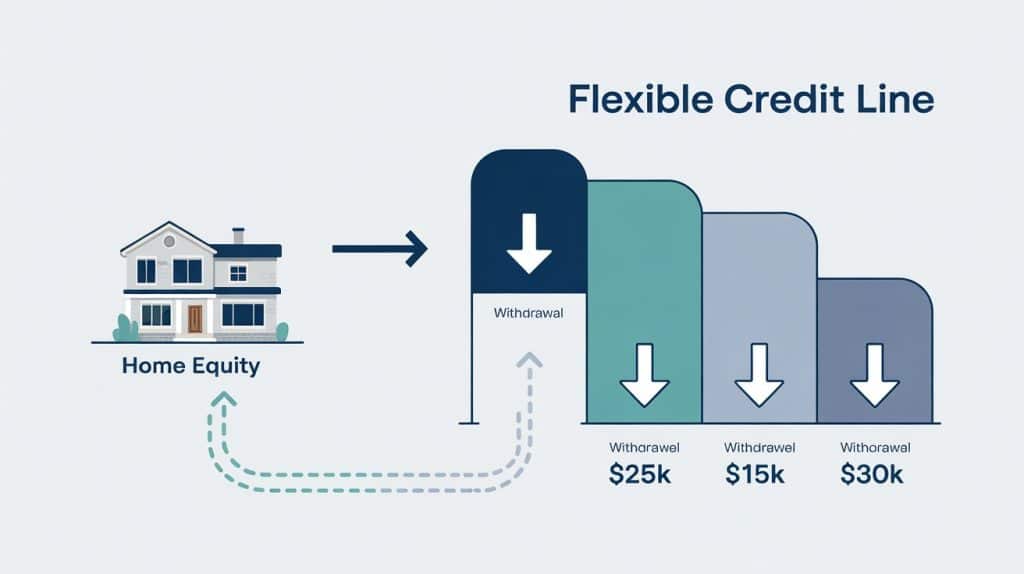

Home Equity Line of Credit

How a HELOC Differs from a Fixed Loan

A home equity line of credit works more like a flexible line of credit than a standard loan.

You are approved for a borrowing limit based on your available equity, but you draw funds only as needed.

Interest is charged solely on the amount drawn, not the full approved limit.

Here’s the sentence broken into two for better readability:

This makes it one of the more cost-efficient options for homeowners who need funds over time rather than all at once.

It’s especially useful for phased renovation projects or as a financial buffer during periods of uncertainty.

You are not paying interest on money sitting unused.

The Variable Rate Risk

Rates on these facilities are typically variable, so repayment amounts can shift when base rates change.

Before committing, run the numbers under a scenario where rates rise by 2 or 3 percentage points to confirm the repayments remain manageable.

Equity Release: Mortgages & Reversion Plans

Who These Products Are Designed For

Equity release products are designed for older homeowners, typically those aged 55 and above.

These products allow them to access the value locked in their property without taking on monthly repayments.

There are two main forms to understand.

Lifetime Mortgage

A lifetime mortgage is a loan secured against your home with no monthly repayments required.

Interest compounds on the original loan and any previously accrued interest, with the full balance repaid from sale proceeds after death or a move into long-term care.

A $50,000 loan at 5% interest, for example, grows to over $81,000 in ten years without repayments.

Most plans include a no-negative-equity guarantee, and some allow voluntary partial repayments each year to keep the balance manageable.

Home Reversion Plan

A home reversion plan involves selling a share of your property, usually below market value, to a provider in exchange for a lump sum or regular income.

You keep the right to live there rent-free for life, and the provider collects their share when the property is eventually sold.

Both products reduce your estate value and carry higher long-term costs than conventional borrowing.

They are best suited to asset-rich homeowners with limited income.

Independent regulated advice is essential before committing to either.

Downsizing

The Cleanest Way to Access Equity

Selling your current home and buying a smaller or less expensive property is the cleanest way to access equity. There is no loan, no interest, and no compounding debt.

If your goal is to pass the property to a family member rather than access cash for yourself, the process follows a different legal path with its own tax and ownership considerations.

The options available, from outright gifting to placing the home in trust for a child, carry different inheritance tax and capital gains consequences depending on the structure of the transfer.

Factor in the Transaction Costs

The costs involved are real and should be calculated carefully.

Agent fees, conveyancing, taxes on the new purchase, and moving expenses can collectively absorb a significant slice of the equity released.

These need to be accounted for before treating a downsize as a straightforward windfall.

On the positive side, moving to a smaller property typically reduces ongoing costs.

Lower energy bills, lower insurance premiums, and lower maintenance costs add up meaningfully over time, alongside the lump sum released at sale.

Which Option is Actually the Cheapest?

A General Framework for Comparing Options

The right choice depends on your circumstances, but a few principles hold across most situations.

Remortgaging at the end of a fixed-rate term typically offers the lowest rates with no early repayment penalties.

A further advance is often cheaper and short-term, when switching lenders would trigger those charges.

A HELOC costs less than a fixed equity loan when you draw funds gradually.

Equity release carries the highest long-term cost due to compounding, though it may be the only viable route for older homeowners with limited income.

Downsizing has the highest upfront costs but removes ongoing interest entirely.

Safe is Not the Same as Cheap

The safest option in every case is whichever one you can genuinely sustain.

Repayments should remain comfortable if your income dips or rates rise.

Borrowing against your home always carries the risk of repossession if you fail to repay.

That reality does not make equity access a poor decision, but it does mean affordability should be assessed conservatively rather than optimistically.

Practical Steps Before You Commit

Taking a little time to prepare before you access equity can save you a surprising amount of money. Here are the key steps to work through first.

Step 1: Get an Independent Property Valuation

Your equity figure is only as accurate as your property’s current value.

An independent valuation reflects real market conditions rather than an estimate you pulled from a listing site, and it gives your lender a credible number to work from when assessing your application.

Step 2: Check Your Existing Mortgage Terms

Carefully review your current mortgage agreement before choosing a route.

Early repayment charges can be substantial if you are still within a fixed-rate period, and they can quickly cancel out any savings you expected from switching products.

Knowing your exit costs upfront lets you time your move correctly.

Step 3: Review Your Credit Report

A stronger credit position unlocks better interest rates across all product types, from remortgages to second-charge mortgages.

Pull your report before you apply, check for any errors, and give yourself time to resolve any issues rather than discovering them mid-application.

Step 4: Speak to a Whole-of-Market Mortgage Broker

Your existing lender will only show you their own products.

A whole-of-market broker compares options across all lenders and can tell you whether a further advance, a remortgage, or a different product entirely gives you the better deal once all fees are factored in.

Step 5: Know When the Goal Is a Transfer, Not a Cash Release

If your goal is to transfer equity to a family member rather than access cash for yourself, the process follows a different legal route.

Many people attempt it without professional help to save on fees, but the consequences of getting the paperwork wrong, especially where a mortgage sits on the property, can be costly to unpick.

Equally, the tax treatment changes significantly depending on whether you are gifting the home outright, selling it below market value to a child, or adding them as a co-owner.

Final Thoughts

No single method works for every homeowner.

The right route depends on your age, income, equity held, mortgage terms, and what you need the funds for.

What matters is understanding the full cost of each option before you commit.

Compare properly, take independent advice, and treat your home equity with the care it deserves.

When used wisely, it opens opportunities. When rushed, it leads to issues that are difficult to undo.

Frequently Asked Questions

How much would a $50,000 home equity loan cost per month?

Monthly payments depend on the interest rate and term. At 8% for 15 years, expect about $480/month; shorter terms increase payments but reduce total interest.

Is a HELOC better than A Home Equity Loan?

A HELOC offers flexible borrowing and variable rates, while a home equity loan provides a fixed rate and predictable payments. The better option depends on your financial needs and rate tolerance.

Can a 70-Year-Old Get a 20 Year Mortgage?

Yes, age alone doesn’t disqualify you. Lenders evaluate income, credit, and ability to repay, not life expectancy, when approving a 20-year mortgage.