Most buyers ask the same question before they sign anything: Is this a good rate? That’s fair. And right now, in 2026, it’s harder to answer than it sounds.

Rates have moved more times in the past year than most buyers expected. Lock in at the wrong time, and you’re paying hundreds more per month than someone who waited a few weeks.

This guide breaks down what a “good” mortgage rate looks like today. You’ll see the current averages, what pushes your personal rate up or down, and what a lower rate actually saves you over 30 years.

By the end, you’ll know what number to aim for and whether the rate in front of you is worth taking.

What Are Today’s Average Mortgage Rates in 2026?

As of April 2026, the average 30-year fixed mortgage rate is roughly 6.30%, according to Freddie Mac’s weekly survey.

Bankrate puts it at 6.33%. Zillow shows the average closer to 5.99%, depending on the lender and borrower profile. The 15-year fixed rate is averaging around 5.50% to 5.65% across major lenders.

These numbers vary because lenders price risk differently. Your personal rate will depend on your credit score, down payment, and loan type.

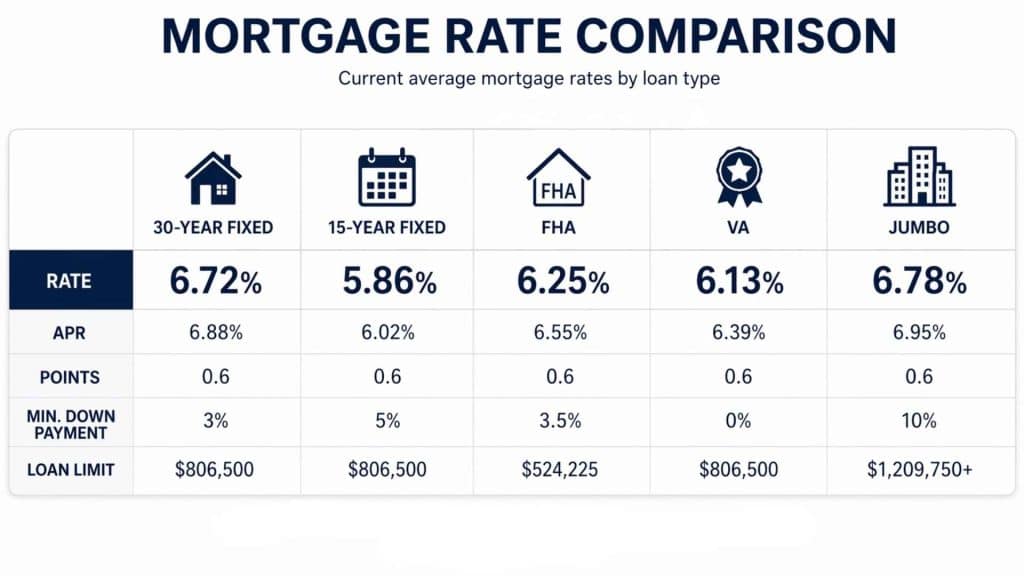

Quick snapshot by loan type (April 2026):

| Loan Type | Avg. Rate |

|---|---|

| 30-year fixed | ~6.30% |

| 15-year fixed | ~5.50–5.65% |

| 5/1 ARM | ~6.17% |

| 30-year FHA | ~6.03% |

| 30-year VA | ~5.57% |

| 30-year Jumbo | ~6.53% |

Rates have fallen from the 7.04% peak reached in January 2025. But they have not returned to anything like pre-2022 levels. Anyone telling you rates are “basically normal” is comparing to the wrong baseline.

What Is a “Good” Mortgage Rate in 2026?

There is no single right answer. A good rate depends on three things: the market average, your loan type, and your personal financial profile.

That said, here is a working guide for 2026:

- Under 6.00%: Excellent. You are below the national average. Very few borrowers get here without strong credit and a large down payment.

- 6.00% to 6.30%: Good. This is the competitive range right now. Most well-qualified buyers land here.

- 6.30% to 6.75%: Average. Acceptable, but worth shopping around. You may be leaving money on the table.

- Above 6.75%: higherthan necessary for most borrowers. Check your credit score before locking.

For VA loan borrowers, anything under 5.75% is worth taking. FHA borrowers around 6.00% are doing fine relative to the market.

The Mortgage Bankers Association predicts 30-year rates will hover between 6.1% and 6.3% for most of 2026. Fannie Mae forecasts rates near 6.0% by year-end.

J.P. Morgan, on the more cautious end, does not expect any Fed rate cuts in 2026.

That context matters. Waiting for 5% rates means waiting until 2027 or 2028, and that is the optimistic scenario.

7 Factors That Determine Your Personal Mortgage Rate

Your rate is not set solely by the market. Lenders look at you as a borrower and price risk based on what they see. Here are the seven main factors that affect what you’re offered.

| Factor | What It Means | Impact |

| Credit score | 760+ gets the best rates. 700 averaged 6.63% in March 2026. Minimum 580 for most loans. | Highest |

| Down payment | 20%+ removes PMI and lowers your rate. Less down means a higher rate. | High |

| Loan type | VA = lowest rates. FHA = 580+ score. Jumbo (above $832,750) = highest rates. | High |

| Loan term | 15-year rates are lower than 30-year rates. Monthly payments are higher, though. | Moderate |

| DTI ratio | Lower monthly debt vs income = better rate offer from lender. | Moderate |

| Points | Pay 1% upfront to cut the rate by ~0.25%. Only worth it if you stay long-term. | Moderate |

| Market | Fed policy, inflation, and global events set the baseline. You can’t control this. | External |

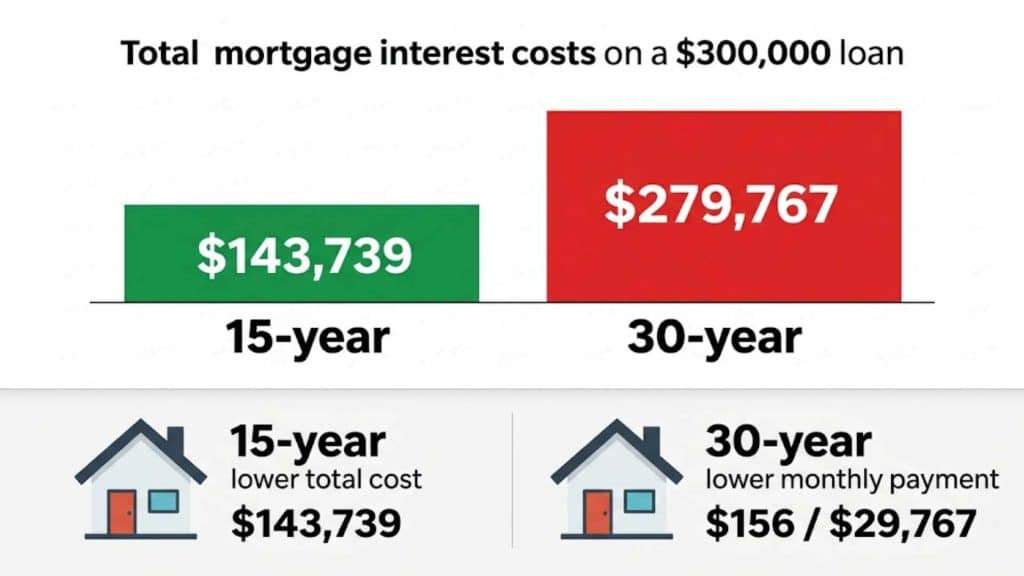

15-Year vs. 30-Year: Which Actually Makes More Sense?

This comes down to what you can afford each month and how much you care about the total interest you pay.

A 30-year fixed at 6.02% on a $300,000 loan costs roughly $1,803 per month (principal and interest). Over the life of the loan, you would pay about $348,904 in interest.

A 15-year fixed at 5.50% on the same loan brings monthly payments up noticeably but total interest drops to roughly $142,228. That is a difference of over $206,000.

The catch is that the 15-year monthly payment is much higher. If that stretches your budget too thin, a 30-year loan with occasional extra payments may make more sense.

The monthly cost also varies significantly depending on how much you borrow. A $300,000 loan and a $700,000 loan at the same rate look very different on a monthly budget.

How Does Credit Score Affect Your Rate In Real Numbers?

The difference between a good and a poor credit score is not abstract. It shows up in your monthly payment and compounds over 30 years.

Bank of America’s example, using myFICO.com data, shows that on a $300,000 30-year fixed loan.

The gap between a score in the 760–850 range and one in the 620–639 range can cost you over $91,757 in extra interest over the life of the loan.

For a $500,000 mortgage, data from mortgage-info.com puts the difference between a 620 and a 780 score at $72,000 or more in additional interest.

What actually moves your credit score before you apply:

- Pay every bill on time, every month. Payment history counts for 35% of your FICO score

- Keep credit card balances below 30% of your limit; aim for 10% or less if you can

- Avoid opening new credit accounts in the months before applying

- Check your credit report for errors well in advance they can take weeks to resolve

What Will Mortgage Rates Do for the Rest of 2026?

Nobody can say for certain. But here is what the major forecasters are currently projecting:

- Fannie Mae: Rates near 6.0% through the rest of 2026

- Mortgage Bankers Association: Between 6.1% and 6.3% for most of the year

- National Association of Home Builders: Average of 5.99% for 2026

- Wells Fargo: Average of 6.14% across 2026

- J.P. Morgan: No Fed rate cuts in 2026

The Federal Reserve held the benchmark rate at 3.50%–3.75% at its March 2026 meeting. As of April 2026, markets are pricing in roughly one cut for the full year.

Fed Chair Jerome Powell’s term ends in May, which adds uncertainty to the picture.

Rates are not expected to fall sharply in the near term. If you find a rate that fits your budget, the case for locking it in is stronger than waiting.

How to Get a Lower Mortgage Rate in 2026?

You cannot control what the market does. But you can control how you look to lenders.

Before you apply:

- Get your credit score above 740 if possible

- Reduce existing debt to lower your debt-to-income ratio

- Save toward a 20% down payment to avoid PMI

- Review your credit report for errors early, not the week before you apply

When you shop:

- Get quotes from at least three lenders. Freddie Mac data shows that borrowers who get just one extra quote save an average of $600 over the life of the loan. Three quotes can save up to $1,200.

- Compare APRs, not just the stated interest rate. APR includes lender fees and gives a truer comparison

- Ask about discount points and do the math on whether buying down your rate makes sense, given how long you plan to stay

Loan type matters more than people realize. The average 30-year VA rate in April 2026 is around 5.57%, well below the conventional average. If you qualify, that difference adds up fast.

How Your Mortgage Rate Connects to What You Can Afford?

Your rate directly affects the price range you can realistically consider.

At 6.30%, the monthly payment on a $400,000 loan is roughly $2,484 (principal and interest). At 7%, that same loan costs around $2,661 per month.

That is a $177 difference every single month, or more than $63,700 over the life of the loan.

That gap is why knowing your rate early matters. It is the number that decides whether a $400,000 home fits comfortably in your budget or whether $350,000 is the more realistic target.

Salary plays into this, too. Most lenders use your gross income to set the ceiling on what they will approve. A household income of $100,000 sits at a very specific point on that scale; it gets you into some price ranges comfortably, but a $600,000 home on that salary is a different conversation entirely, one that usually involves a co-borrower, a large down payment, or both.

For buyers looking at the full cost of owning a property, including the cost of buying the freehold on a leasehold home, a freehold purchase calculator puts those numbers alongside mortgage figures.

Conclusion

A good mortgage rate in 2026 sits between 6.00% and 6.30% for most buyers with solid credit. VA borrowers can do better.

Those with lower scores will generally pay more often by a larger margin than they expect, unless they work on their profile before applying.

Rates are not expected to fall sharply this year. Most forecasts keep the 30-year fixed in the 6.0%–6.3% range through the end of 2026. The case for waiting on a big rate drop is weaker than it looked six months ago.

Know your credit score. Get multiple quotes. Now, what a small rate difference actually costs over 30 years. Those three steps alone put you in a better position than most buyers walking into a lender’s office.

What rate are you seeing from lenders right now? Drop it in the comments; it helps other buyers know what is actually being offered out there.

Frequently Asked Questions

What Is a Mortgage Rate Lock Float-Down?

A float-down option lets you lock in a current rate while still snagging a lower one if market interest rates drop significantly before your home loan officially closes.

Can I Get a Mortgage with A 1099 Income?

Yes, but lenders usually require two years of consistent self-employment history. They will average your net income from tax returns to determine your specific debt-to-income ratio and eligibility.

How Does a Mortgage Recasting Work Exactly?

Recasting involves paying a large lump sum toward your principal. The lender then recalculates your monthly payments based on the new balance, keeping your original interest rate and term.

What Are the Benefits of A Portable Mortgage?

A portable mortgage allows you to transfer your current interest rate and loan balance to a new property, which is incredibly valuable if your existing rate is lower than current market averages.

Does a “no-Closing-Cost” Mortgage Actually Save Money?

Not necessarily. The lender covers upfront fees in exchange for a higher interest rate or by folding the costs into the loan balance, increasing your total interest paid over time.